How Serial Acquirers Turn Into Multibaggers

I’ve read 300 pages so you don’t have to. Here's why serial acquirers produce so many multibaggers, distilled from the best study ever written on them.

To read our full disclaimer, click here:

Last week I wrote about John Malone, and the $1 invested in his cable empire that turned into more than $900 over 25 years. If you missed it, start there - it’s the perfect set-up for this one.

Because here’s the thing I only hinted at last week: Malone wasn’t really a “cable guy.”

He was a serial acquirer.

Over one fifteen-year stretch he did a deal every two weeks, borrowing against the cash flow of the systems he already owned to buy the next one, then the next. The cable just happened to be what he was rolling up.

That same machine - buy a business, improve it, use the cash to buy another, repeat - has been quietly minting multibaggers all over the world.

Not for one lucky operator. For a whole category of companies.

So this week I want to zoom out from the man to the model.

No stock pick today. Instead I’m going to teach you why serial acquirers work, and I’m going to lean on the single best piece of research I’ve ever read on them: a 300+ page study by REQ Capital, a Norwegian fund that does nothing but study these businesses.

I've read all 300 pages so you don't have to. And stick with me to the end - I'll point you to a free list of 100+ serial acquirers from around the world to start your own hunt.

Let me walk you through the parts I underlined…

The Chart That Matters

Start with the scoreboard, because it’s the part most people don’t believe until they see it.

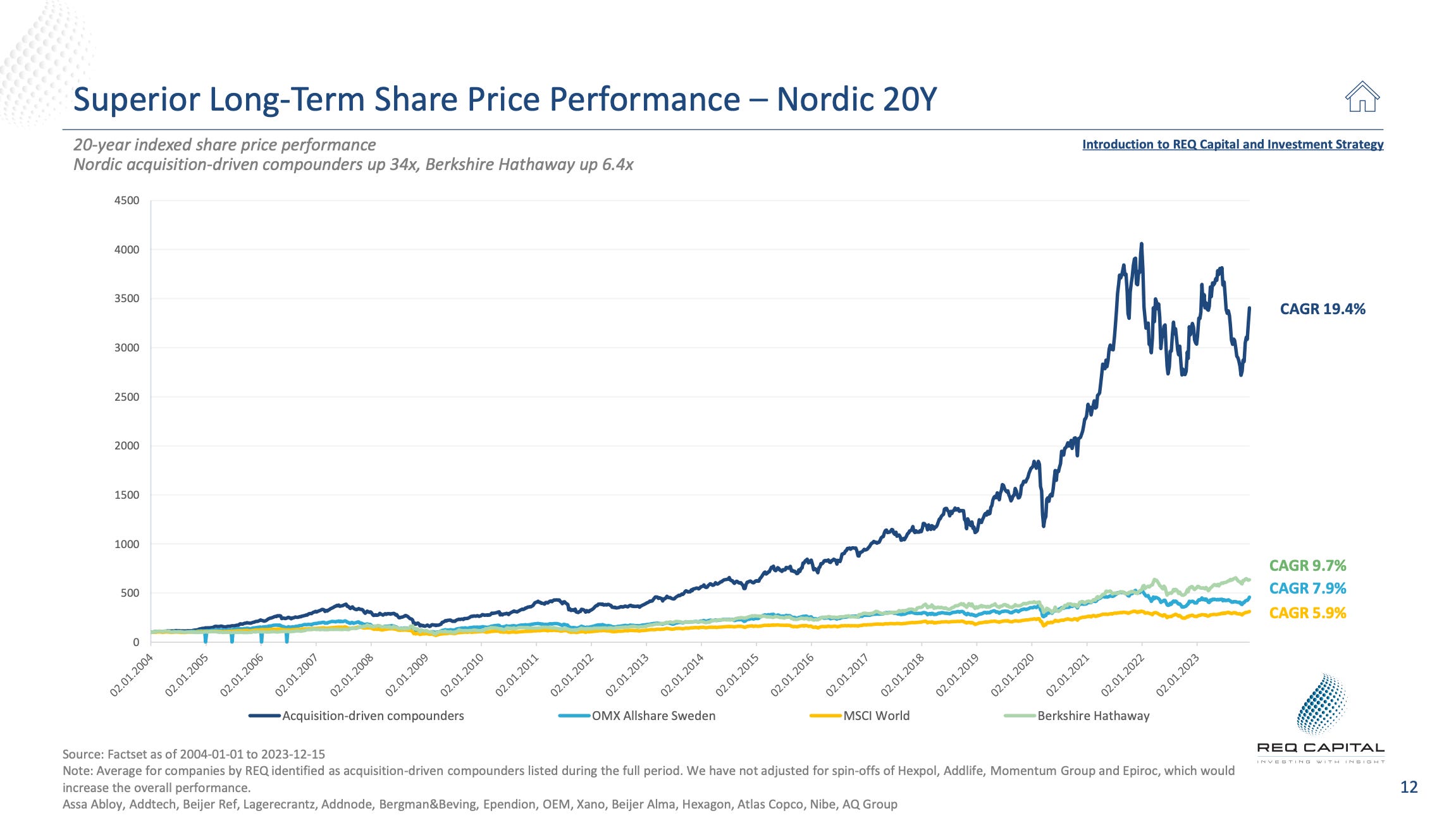

REQ took a basket of Nordic acquisition-driven compounders and indexed their share prices over 20 years. The result: they compounded at roughly 19.4% a year - turning $1 into about $34.

Over the same two decades, the broad global market (the MSCI World) returned about 5.9% a year, and the Swedish market around 9.7%. A basket of these boring, mostly unheard-of acquirers delivered roughly triple the annual return of the global index - for twenty straight years.

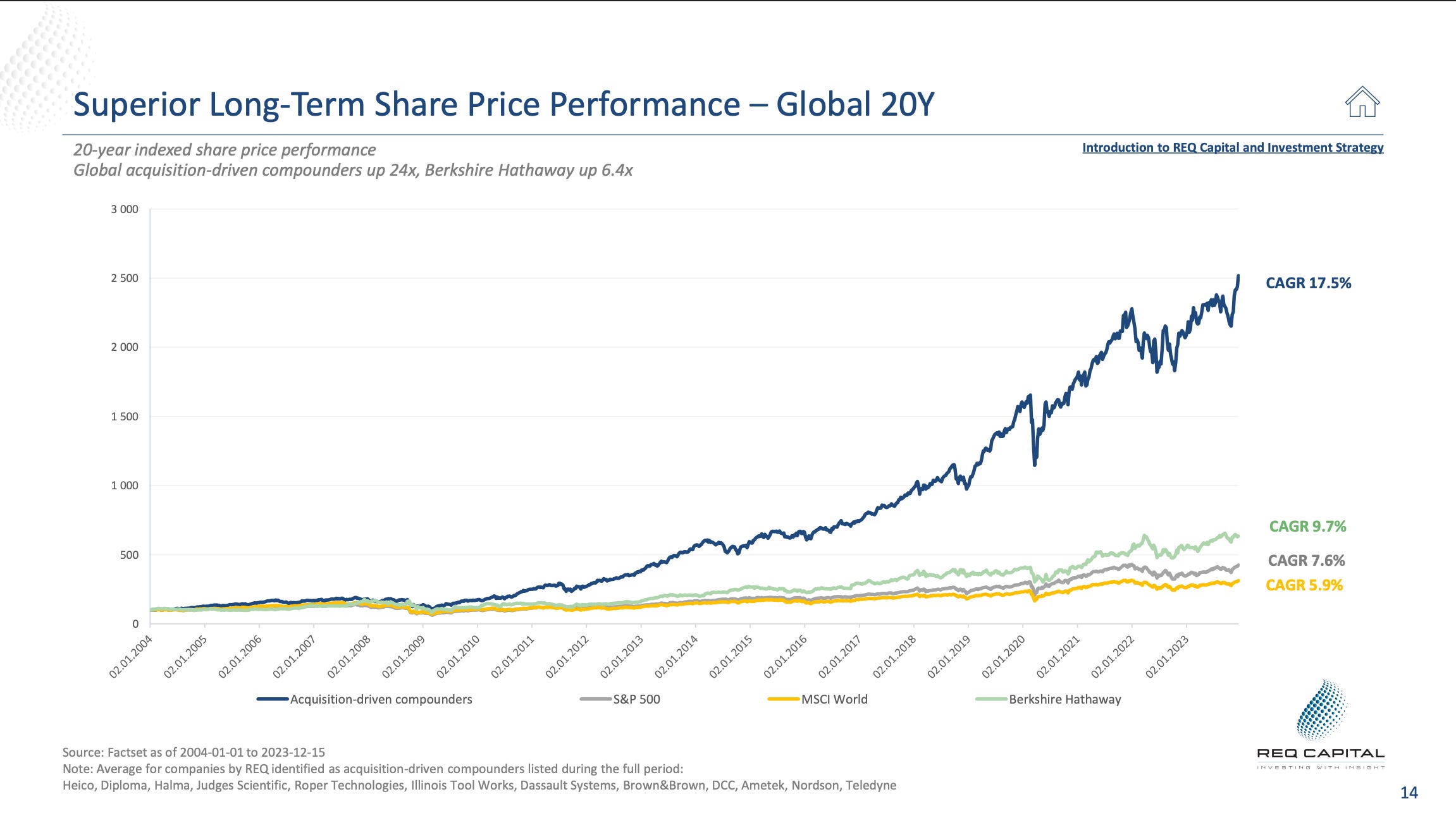

The global basket REQ studied tells the same story - up around 24x over 20 years.

This isn’t one fluke company. It’s a repeatable pattern.

The obvious question is why - and that’s the whole point of today.

A fair caveat before we go on: studies like this look at the survivors, the ones that worked. Plenty of acquirers blow up, and I’ll show you exactly how near the end. But the best of them have produced returns that are genuinely hard to find anywhere else in public markets.

What These Companies Actually Are

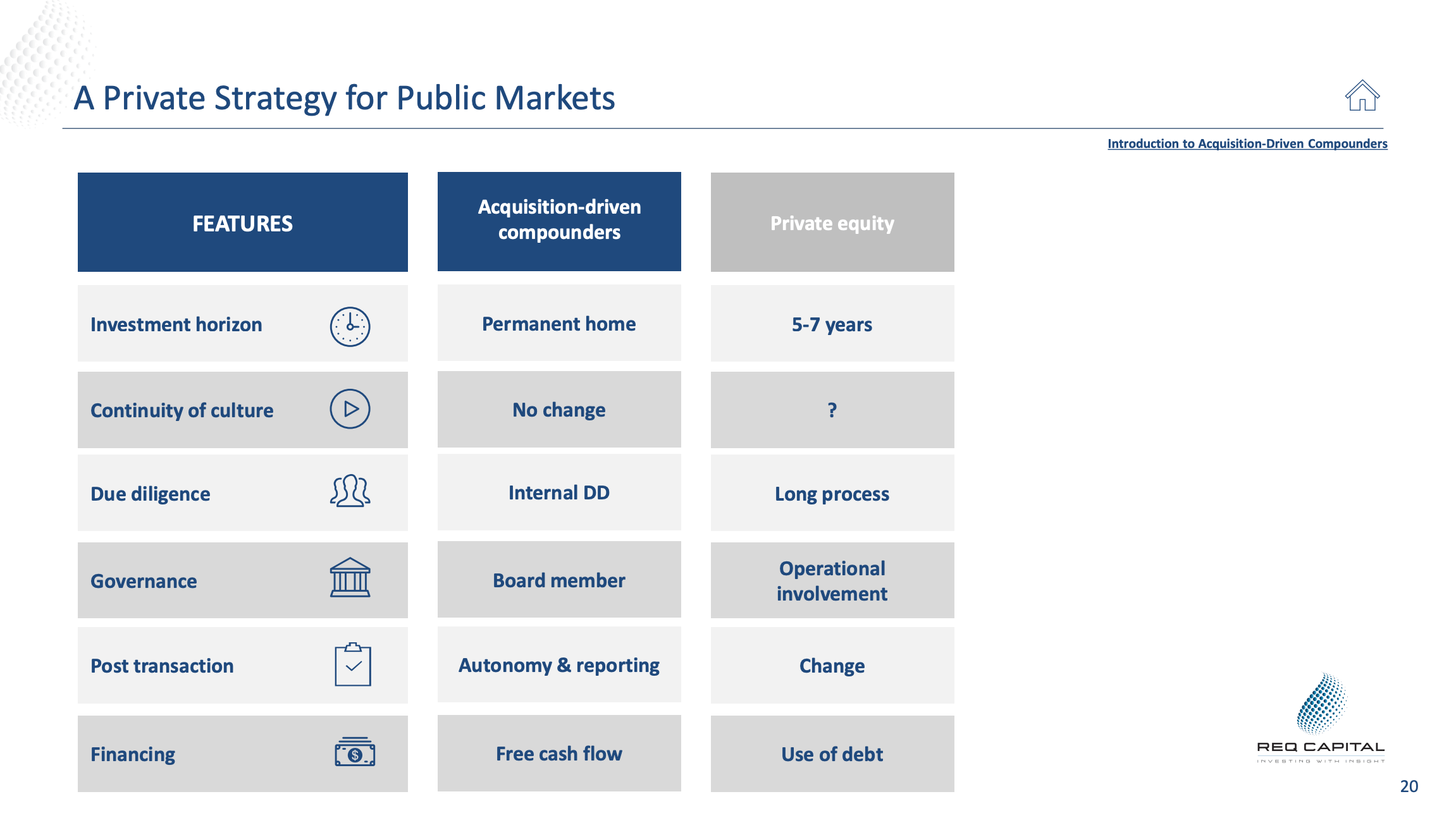

REQ’s definition is simple: a serial acquirer is a company that throws off strong free cash flow and uses it to buy small, often family-owned, private businesses - over and over, as the core strategy.

It’s a private-equity strategy run inside a public company - but without the things that make private equity fragile. No fund that has to sell in five years. No mountain of acquisition debt. Instead: a permanent home for the businesses it buys, funded by cash flow, holding forever.

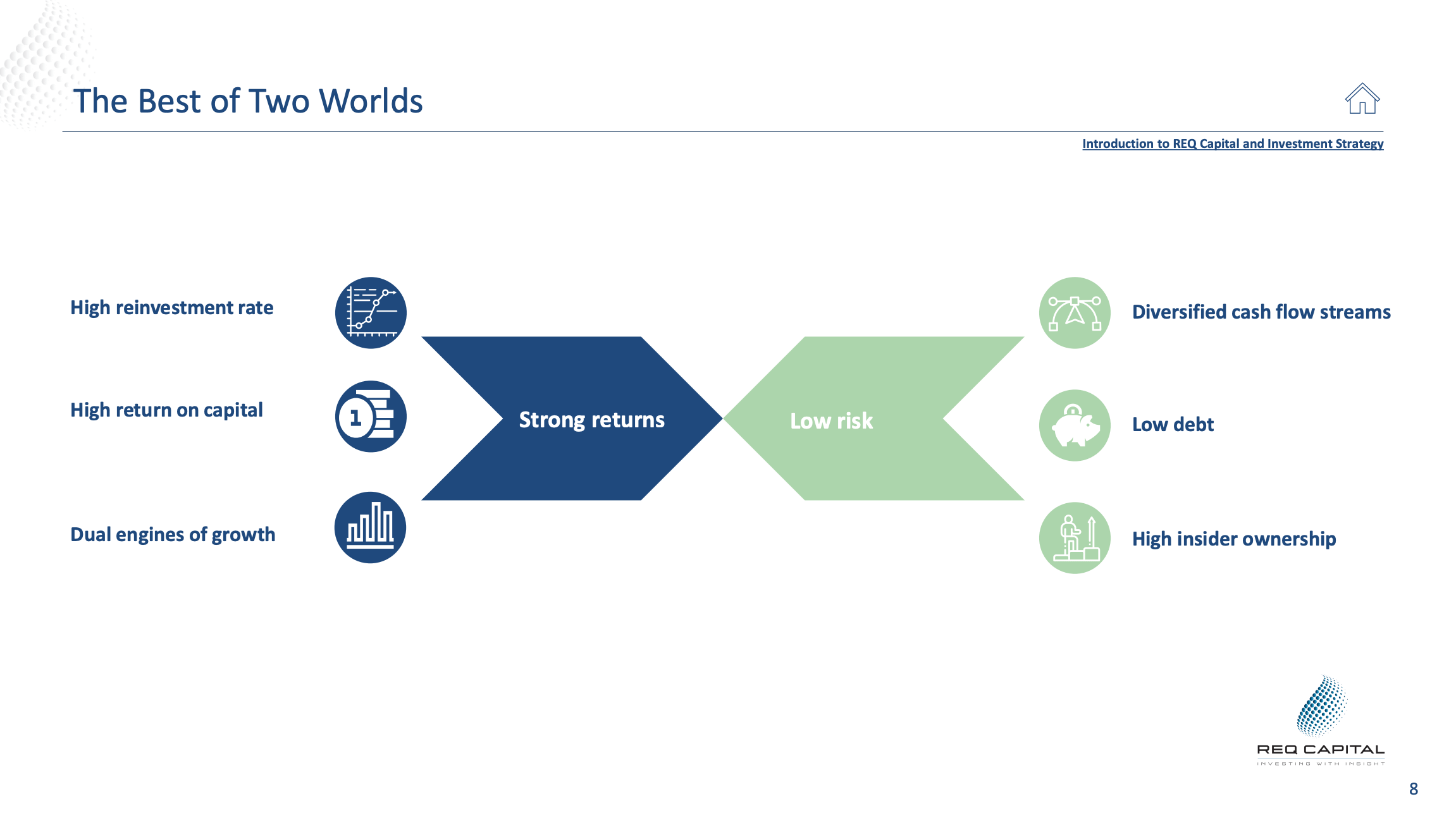

REQ frames the appeal as “the best of two worlds.”

On one side, the things that drive strong returns: a high reinvestment rate, a high return on capital, and dual engines of growth (organic and acquired). On the other, the things that keep risk low: diversified cash flows from dozens of little businesses, low debt, and high insider ownership.

Why The Model Works

Now the mechanics. There are three things doing the heavy lifting, and once you see them you can’t unsee them.

1. They buy cheap - because private is cheap.

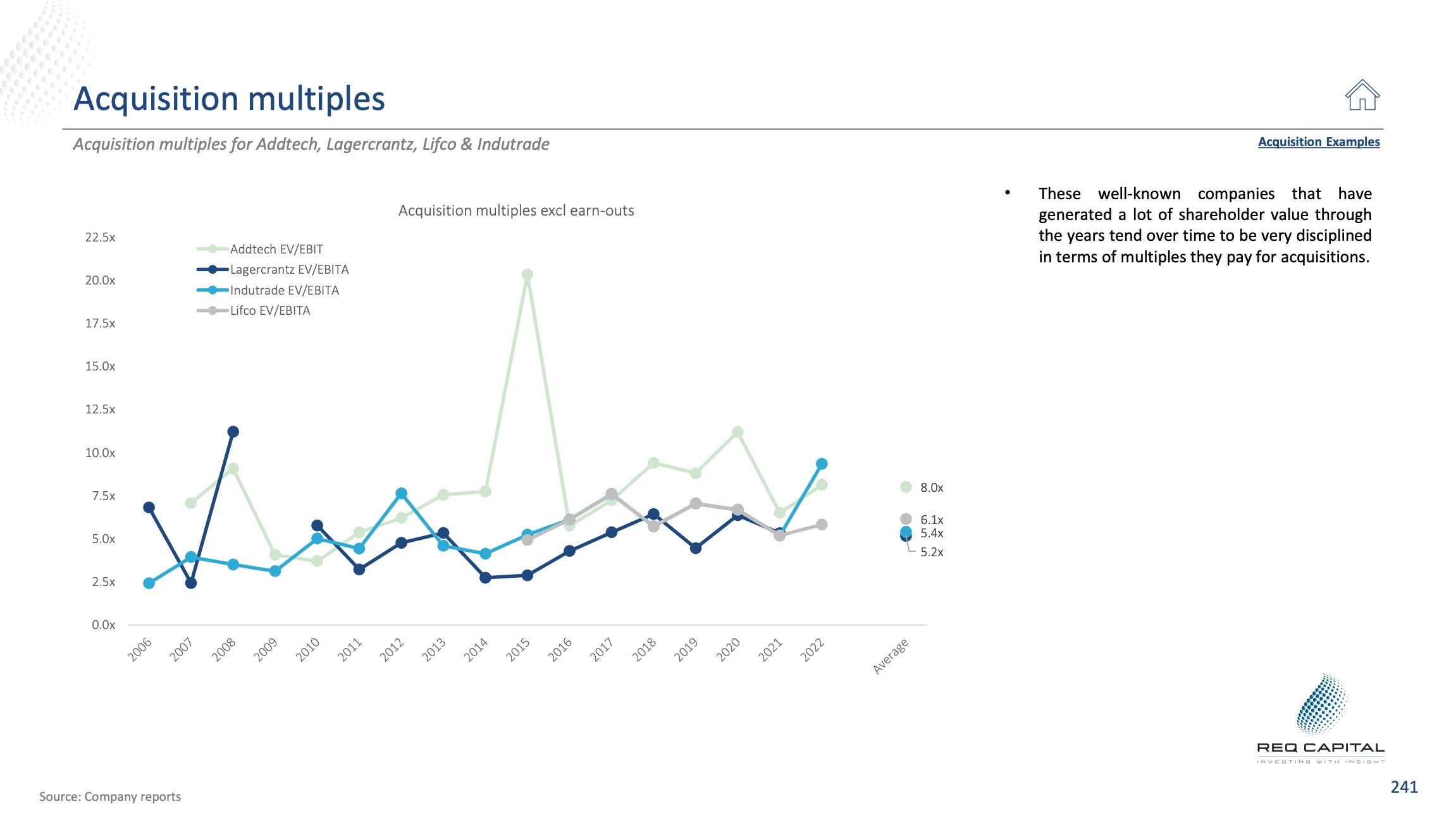

Small private companies sell for far less than public ones. A former Addtech executive put the rule of thumb bluntly in REQ’s study: nobody pays more than 7-8x earnings for a small private business, and for one that depends on a single founder or a few customers, there should be a 30-50% discount. That’s how you end up buying at 5x earnings.

Across the best Nordic acquirers, REQ shows the multiples paid clustering around 5-6x - Lagercrantz near 5.2x, Lifco 5.4x, Indutrade 6.1x. Meanwhile the acquirer itself trades at 15-25x. Buy a stream of profits at 5x while your own shares are valued at 20x and you have created value the instant the deal closes.

2. They reinvest almost everything, at high returns.

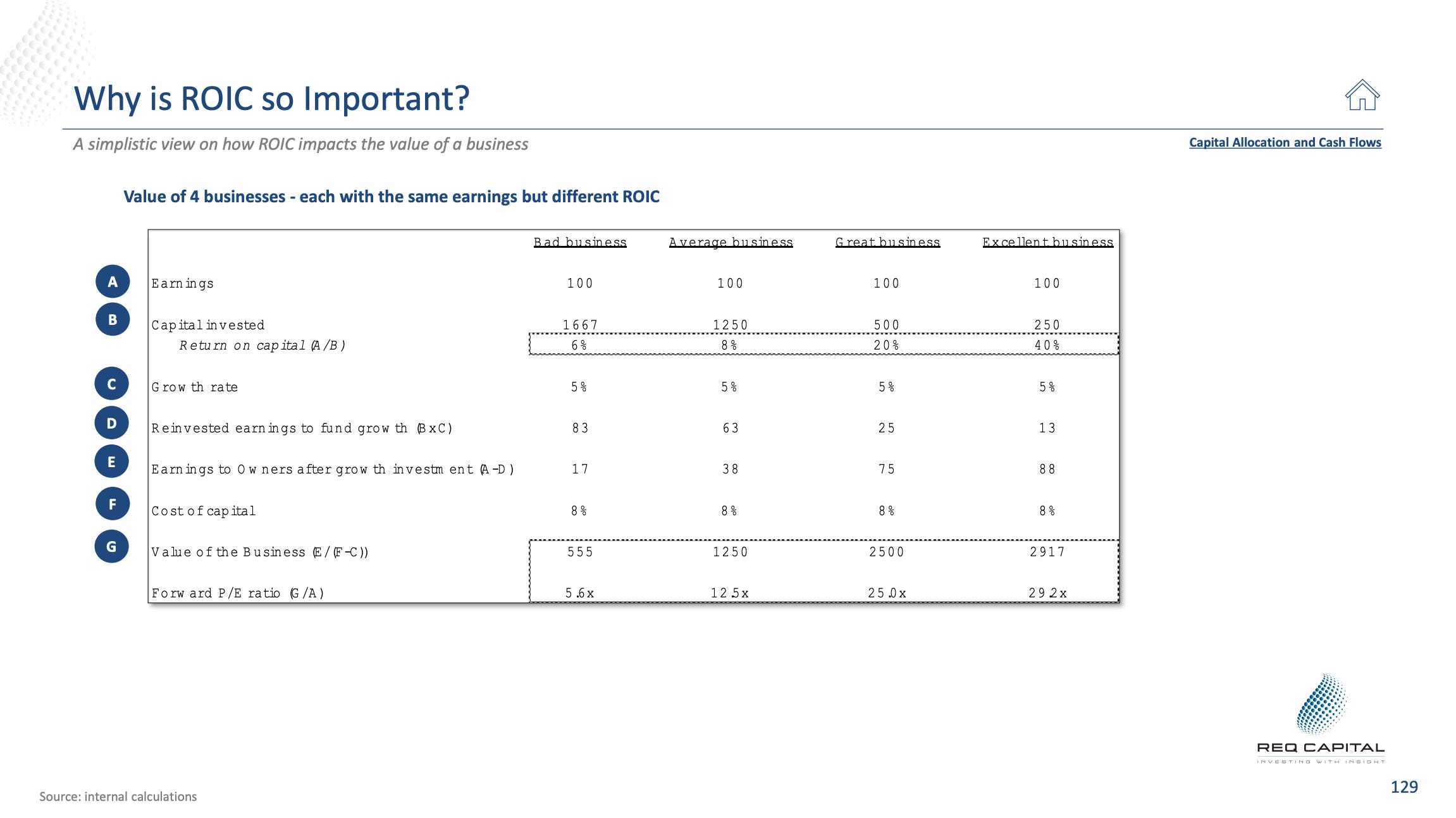

Here’s the engine. Your long-run growth is, roughly, how much of your cash you reinvest multiplied by the return you earn on it. These companies reinvest the vast majority of their cash flow back into more acquisitions, at returns on capital well above the market. REQ’s point on ROIC is the one that matters most here: two companies can earn identical profits, but the one that can redeploy its cash at high returns is worth far more than the one that can’t.

3. The hunting ground barely shrinks.

The fear is always “won’t they run out of companies to buy?” REQ spends a whole section answering it: no. These acquirers fish in markets of thousands of tiny family firms, and an ageing generation of founders is handing over businesses every year. The runway is measured in decades. In multibagger hunting, runway is everything.

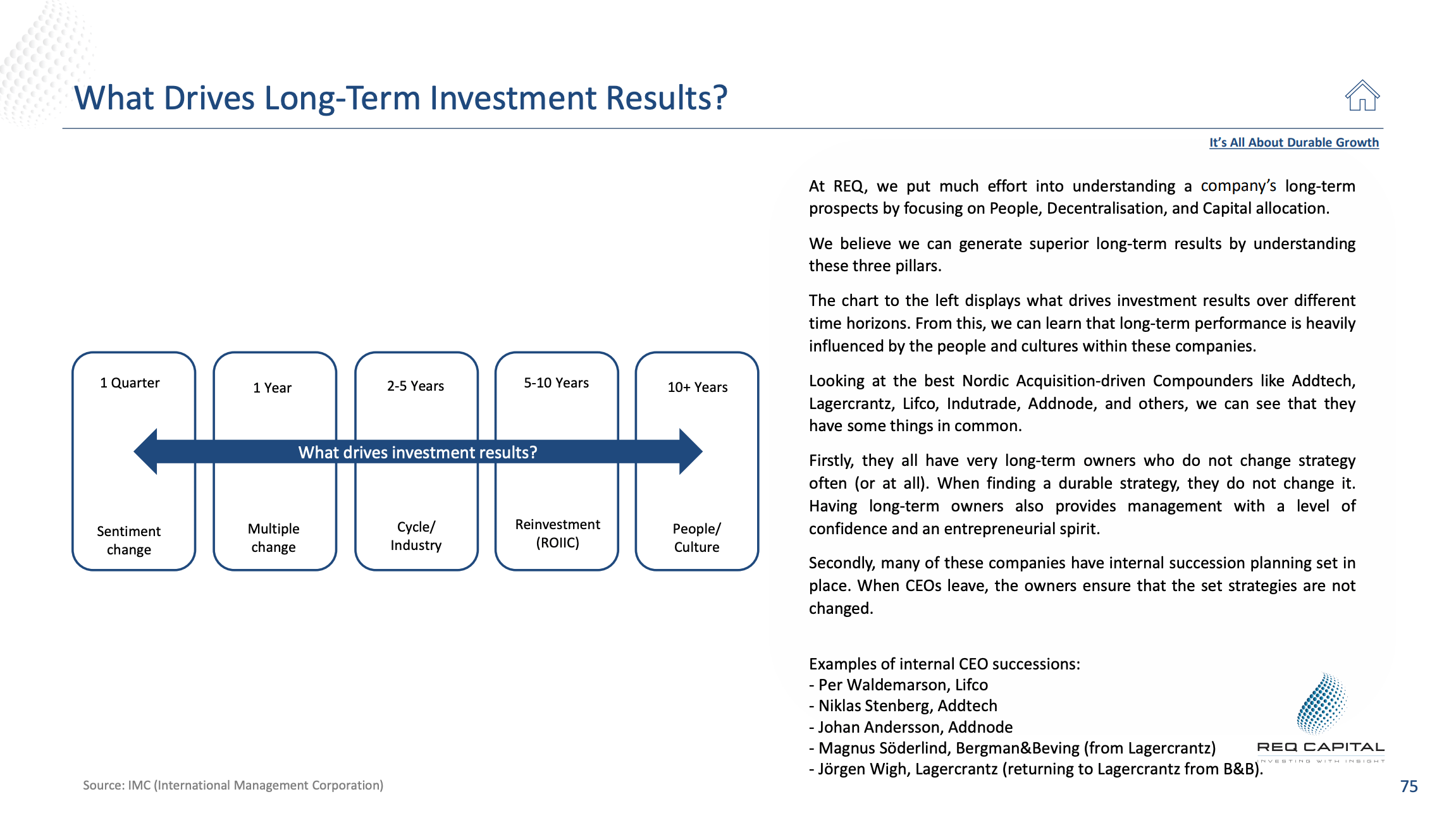

There’s a beautiful REQ slide that ties this all together - what actually drives your return over different time horizons. Over one quarter, it’s sentiment. Over a year, it’s the change in multiple. Over 2-5 years, it’s the cycle. But over 5-10 years it’s reinvestment (return on incremental capital), and over 10+ years it’s people and culture.

The noise that obsesses the market - sentiment, multiples, the cycle - is what matters over months and a year or two. What matters over a decade is exactly what serial acquirers are built to maximise: reinvestment and culture. They are, almost by design, optimised for the only variables that decide long-term returns.

The Three Things That Separate The Great Ones

Not every acquirer is a good one. REQ boils the winners down to three traits that show up again and again, across every country and industry.

Capital allocation. The discipline to treat every dollar as an investment decision - M&A, buybacks, dividends, debt - and only ever do the thing that builds the most value per share. The great ones pay sensible prices and walk away when deals get expensive. They would rather do nothing than overpay. This is the Malone gene exactly: the CEO as full-time investor.

Decentralisation. The best acquirers run astonishingly thin head offices and leave operating decisions to the people who actually run each business. Constellation Software, at enormous scale, famously kept a head office of around 14 people. The most advanced ones push decision-making - even acquisition decisions - down to their operators, so the whole group becomes a network of capital allocators rather than one genius at the top. That’s what lets them keep compounding long after most companies get too big to grow.

People. Founder-operators with their own money on the line, thinking in decades, who don’t play the quarterly guidance game. REQ found CEOs in this group owning stakes worth many multiples of their salary - in some cases over 100x annual pay. When management’s wealth rides on the same shares you own, the incentives finally point the same way. (Sound familiar? It’s the skin-in-the-game point I make in nearly every post.)

Cheap and disciplined with capital. Thin and decentralised in structure. Owner-operators with a long horizon. That’s the lens.

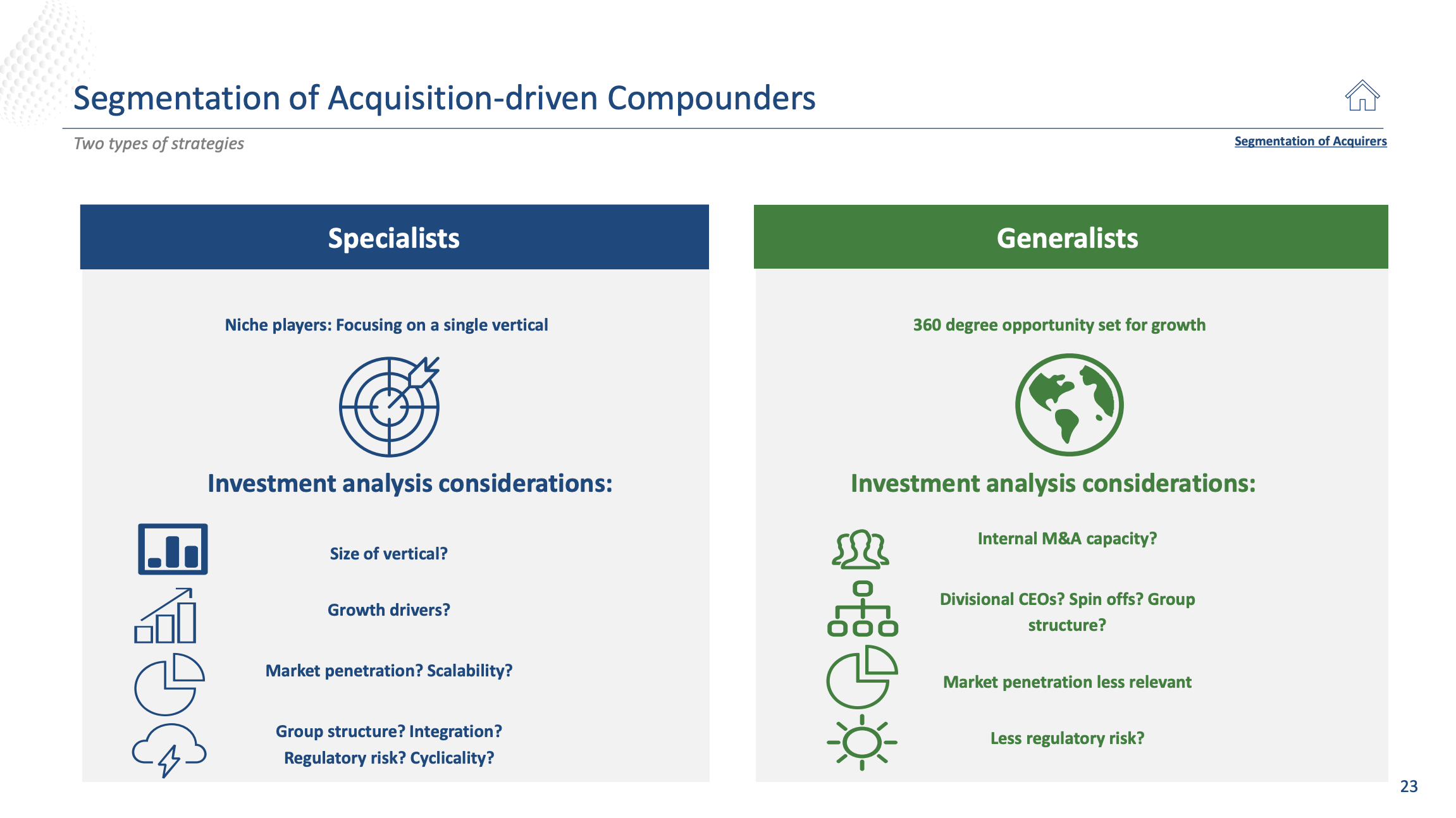

Two Flavours: Specialists and Generalists

One genuinely useful idea from REQ: not all acquirers are the same animal, and you analyse them differently.

Specialists buy within one niche and often integrate more tightly for scale. Their edge is becoming the “buyer of choice” - the obvious home for any founder selling in that space.

Generalists buy good businesses across many industries, judging each on its own merits. Constellation, Halma, HEICO and Danaher live here. Less cost-cutting, but far more runway.

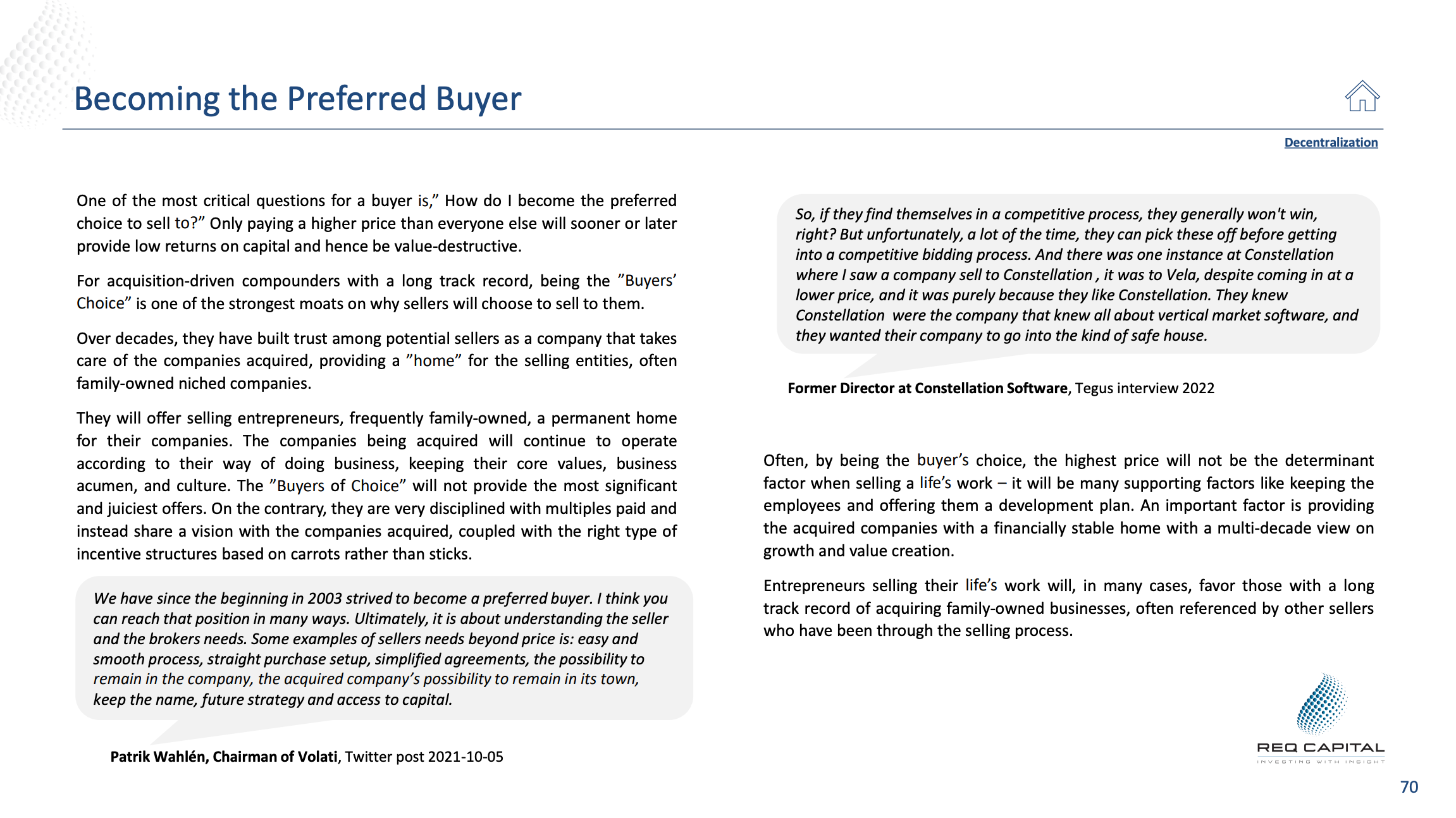

That “buyer of choice” idea is worth dwelling on, because it’s a real and underrated moat. When a founder sells the company they spent 30 years building, the highest bid often doesn’t win.

They care who will look after their staff, their name, their legacy. An acquirer with a permanent home and a track record of not breaking what it buys gets first call - and pays lower prices because it isn’t in a bidding war.

Where The Wheel Comes Off

I won’t sell you this as a free lunch. REQ is refreshingly honest about the failure modes, and so am I.

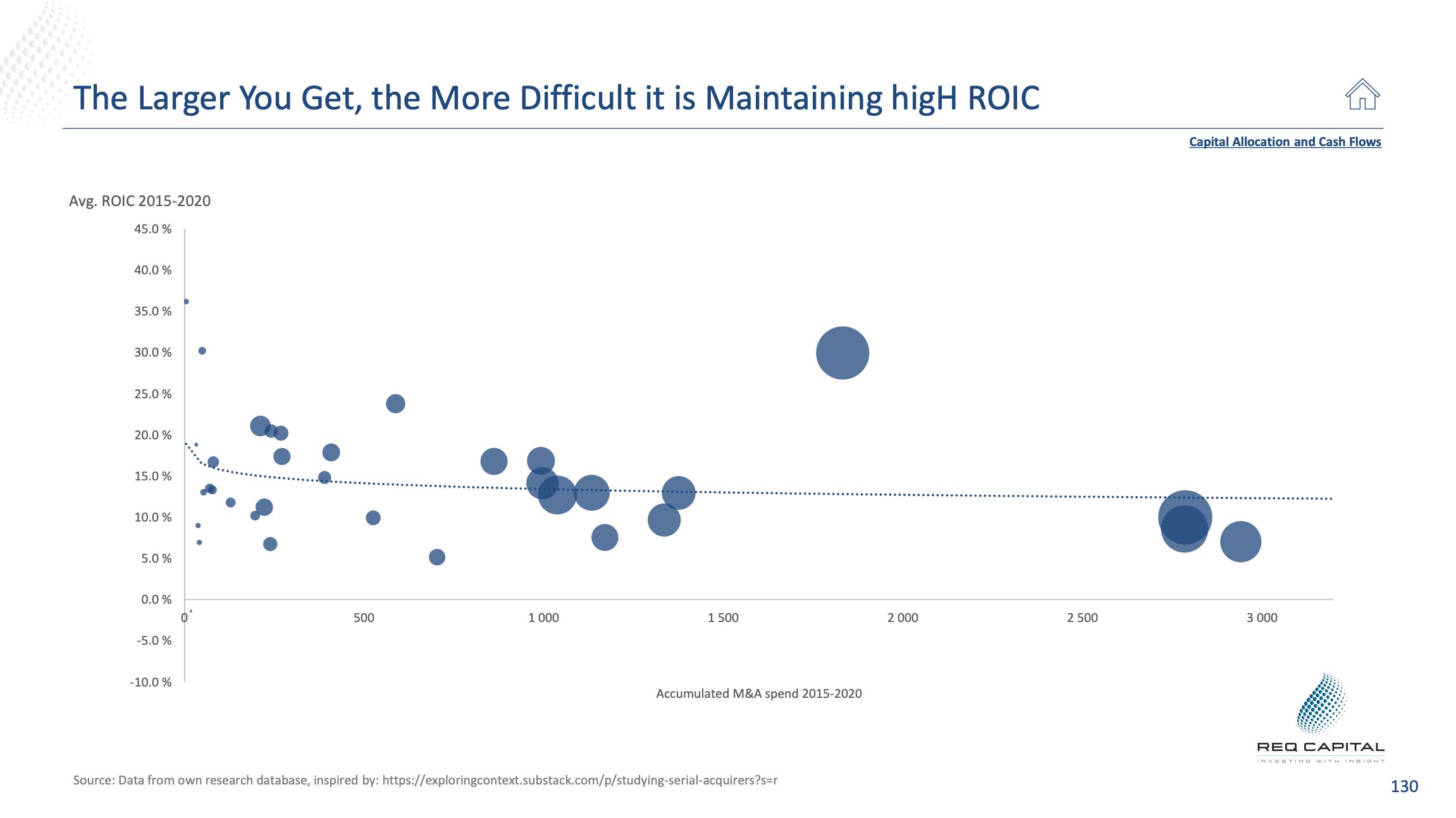

Success itself is the first enemy. The bigger an acquirer gets, the harder it is to keep returns high - small deals stop moving the needle, so it’s pushed into bigger, pricier ones. REQ shows the maths plainly: at scale, the return on capital tends to grind lower.

This is good news for us as small-cap hunters. The model works best while a company is still small and the deals are still tiny - which is exactly the part of the market we live in. The giant compounders everyone already knows are mostly past their highest-octane years.

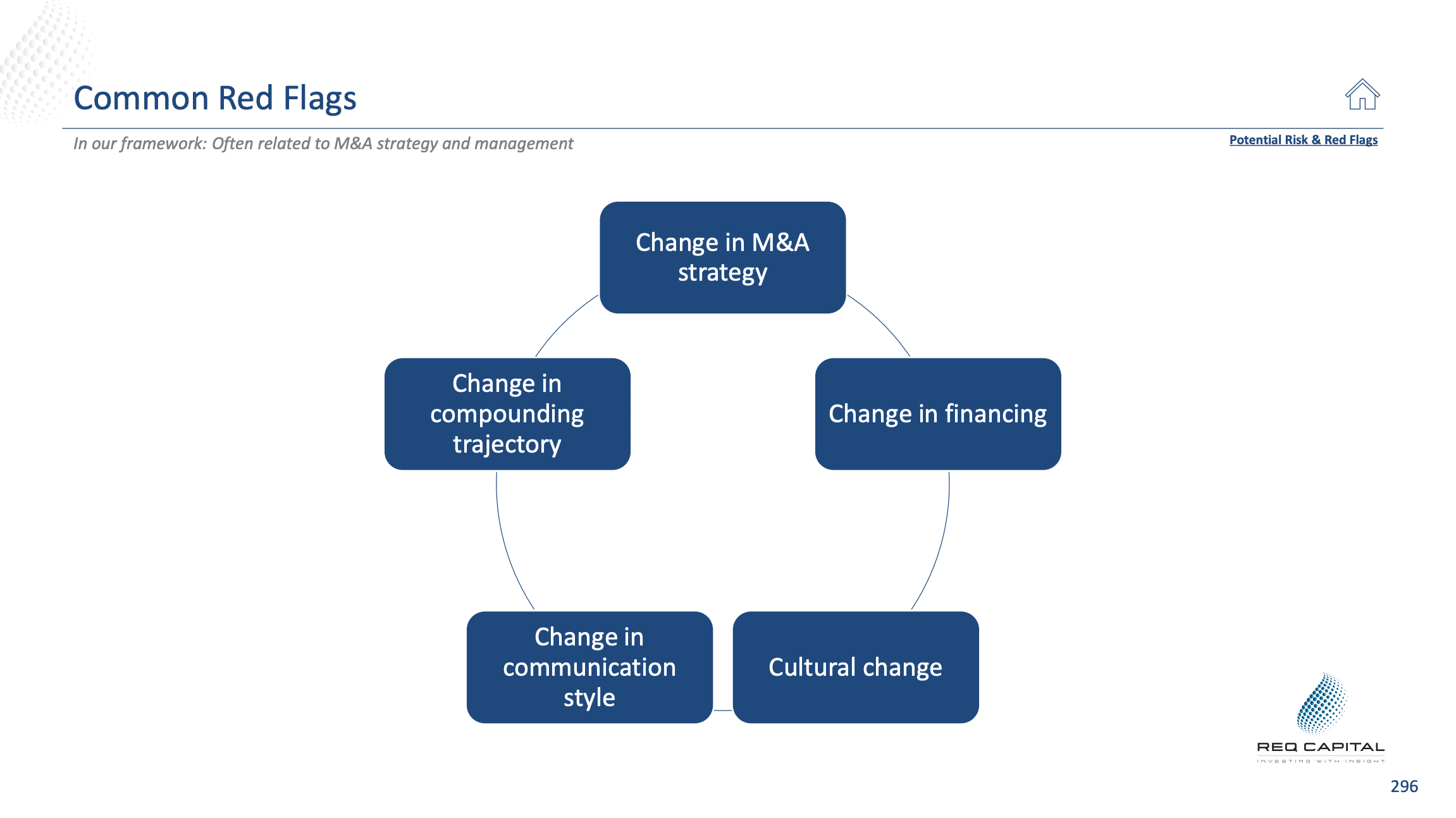

The other failure modes REQ flags are the ones to watch for like a hawk. They group the warning signs into five red flags: a change in M&A strategy, a change in financing (suddenly funding deals with debt or constant share issuance), a cultural change, a change in how management communicates, and a break in the compounding trajectory.

Put simply: the model breaks when discipline breaks. When a great acquirer starts overpaying to keep the growth story alive, leans on debt, centralises until the founders walk, or gets cute with the accounting - that’s your signal, long before the share price tells you.

So the job was never “find a serial acquirer.” It’s find a disciplined one, still small enough to have a long runway. Get that right and time does the rest.

Why I Keep Finding Them

Everything REQ describes - small, ignored, cash-generative, owner-operated, still early on the runway - is the exact fingerprint I hunt for.

It’s the same one Malone left thirty years ago.

So it’s no accident that 9 of the companies I’ve covered run this playbook: vertical-market software, rare-disease drugs, private schools, subsea equipment, recurring-revenue services, fragmented Italian industrials. Different countries, different industries, the same machine underneath - and most still small enough to be in the high-return part of the curve.

How To Use The Two Resources

As promised at the top, here’s the free resource.

A while back I published 100+ Serial Acquirers From Around the World - a running index of acquirers from every geography, the model in action across dozens of industries.

It’s completely free, it’s built as a community project (subscribers and other investors keep adding names), and it’s the single best starting point I know for finding these companies.

That’s your map of the whole world.

The Multibagger Research Portal is where the map turns into research.

Every company I’ve covered lives there in one place, filterable by sector, geography and conviction, each with the tightened thesis and time-stamped updates.

The portal is included free with a paid subscription - subscribe, then log in with the same email. Prices rise later this year now that it's live, and anyone who joins before then locks in today's price for as long as they stay.

Thanks for reading,

Nico

Source: REQ Capital, "A Deep Dive into Shareholder Value Creation by Acquisition-Driven Compounders" (December 2023), authored by Adnan Hadziefendic and Kjetil Nyland. Every chart, data point, and framework referenced above is drawn from that study, and full credit goes to the REQ Capital team for the underlying research. The complete deck is freely available on their website at req.no. If you want to go deeper than I have here, it is well worth your time.

Disclaimer: The Content does not constitute investment advice, financial advice, trading advice, or any other sort of advice. Nothing in this newsletter should be construed as a personal recommendation or advice to buy, sell, or hold any investment or security. All Content is provided for general informational purposes only and should not be relied upon for making investment decisions. You should not make any investment decision based solely on the Content without first consulting with qualified financial advisors, conducting your own research, and considering your individual financial circumstances, investment objectives, and risk tolerance. To read our full disclaimer, click here.